Intel 2030 Financial Model

I know it says 2030, but we'll know Intel's 2030 capacity plans by 2028 due to design decisions and contracts. Plus, why Intel should acquire Substrate for its XRL tool as soon as possible.

Hint, my implied 2026 price target is $118

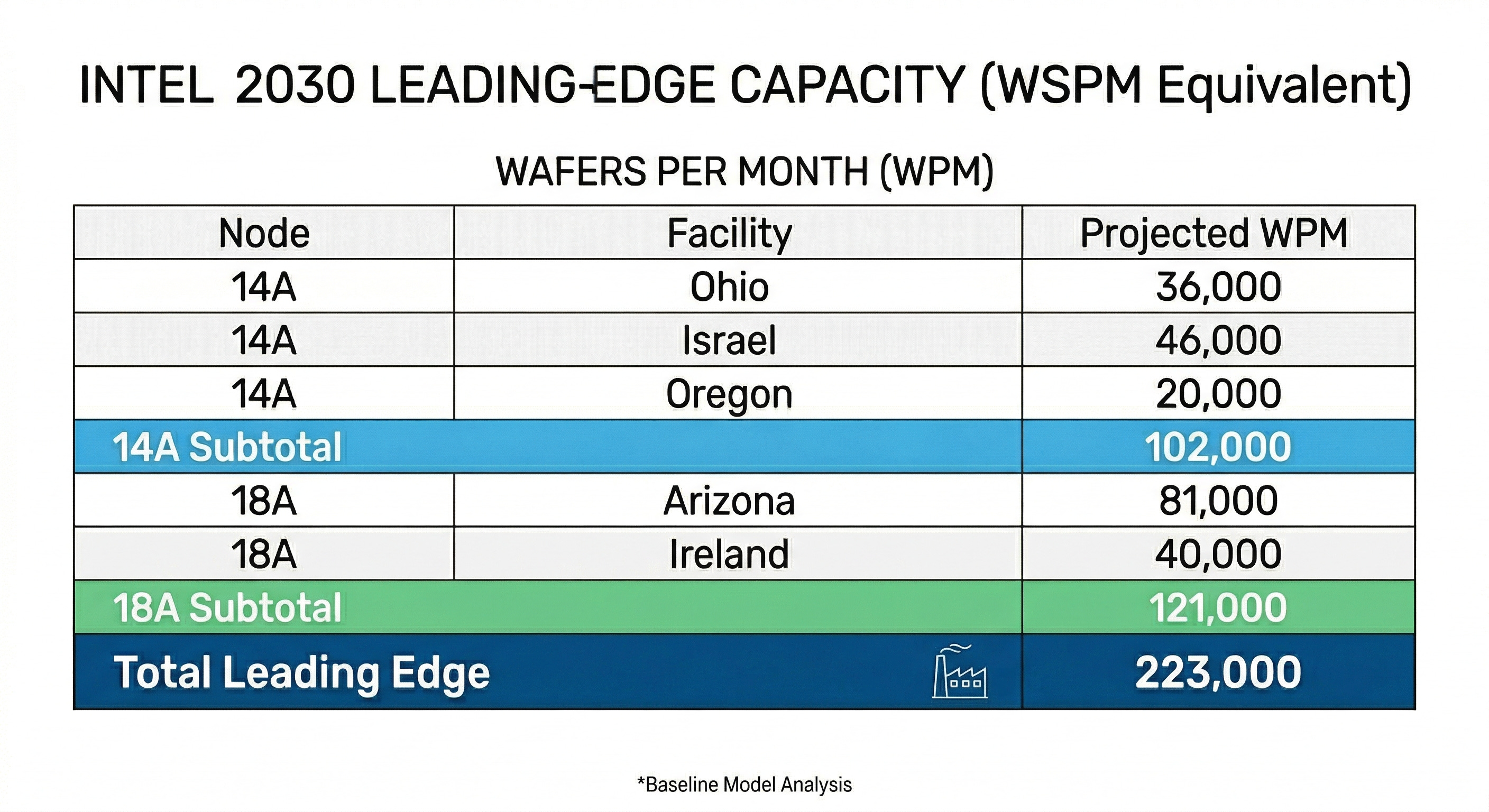

I model Intel producing 145,000 wafers per month in 2025 (if you have different numbers, please let me know). This was a bit of a finger-in-the-air number with some error bars, compared to the max capacity figures, which are very accurate. This 2025 number includes TSMC wafers, 14nm, Intel 7, Intel 3, and Intel 18A. Part of this analysis is judging how much the Intel core business will need wafer growth, considering the PC market is shrinking due to DRAM prices, while Data Center CPU demand is exploding higher. I judge that Intel will need to grow the core CPU wafer business by roughly 22% by 2030. That brings us to roughly 170K wafers. However, even by then, Intel will still be producing Intel 7. I figure roughly 25K Intel 7 wafers and 18K other wafers, which includes Intel 16 and Intel 12. That leaves us with 127K in leading-edge demand.

Now, working on the max capacity figure, I am going to convert Ireland Intel 3 from its 65K WSPM to about 40K WSPM 18A equivalent. I am not judging whether Ireland goes 18A or 14A, or if Intel finds a good business case for 65K Intel 3 wafers in 2030. It just makes the math easier.

Intel has also stated that Oregon will now be doing HVM, which would be roughly 20K 14A wafers in that timeframe.

All of these figures are boosted numbers resulting from Intel deramping Intel 7 in Arizona and Israel to support 18A and 14A. I would be surprised if Intel proceeded with trying a 7nm node. Just boost the leading edge, please!

Read my article to see why Intel can hit these figures

Since Intel’s core business requires 127K WSPM, that leaves us with roughly 100K available leading-edge wafers for external customers or Intel GPUs (no judgment if this works out). I am also saying that, for all practical purposes, Intel has exited attempting to buy leading-edge TSMC wafers at this point. That is likely the reality, given TSMC supply shortages after Nova and Razor N2P orders, which have already been purchased.

To make the math easier, I am going to blend the 18A and 14A ASPs of 23K and 32K, respectively, arriving at a blended 27K.

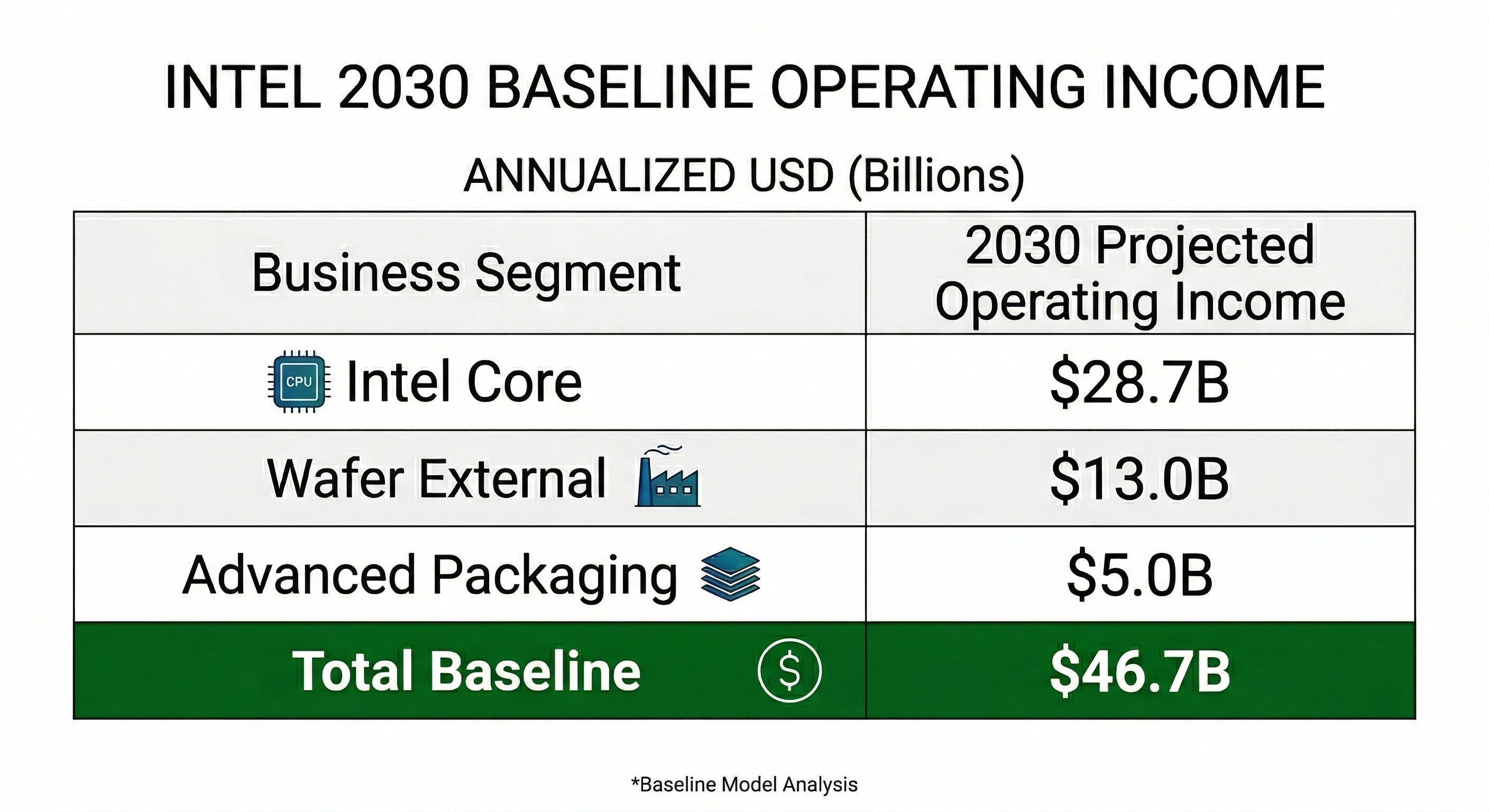

If Intel is consuming 127K WSPM of these wafers, the Intel core CPU business will be doing $82B in 2030. I am going to assume Lip Bu has kept up his hiring of top-tier talent, allowing Intel to achieve 35% operating margins on this business. That gives us $28.7B in operating profit. This should be enough to push the foundry business into slight positive territory, allowing us to treat external orders as new business, aka almost pure gross margin on the tooling and facilities.

For external business, an annualized 100K WSPM * 27K with a 40% gross margin equals $13B in operating profit.

Looking at the Intel Malaysia and New Mexico sites, they should have a similar advanced packaging capacity to what TSMC had in 2025. With additional EMIB efficiencies, I think Intel could offer around $12B worth of advanced packaging capacity. Assuming 40% gross margins, that means $5B in operating profit.

This is just going off that baseline and NOT including any success for Intel ASIC and Intel AI GPU biz, or glass substrates (I have no idea how to model those).

At a 30 PE ratio (if they are actually running at maximum capacity, Intel will be building lots of shells and future growth would be quite strong, justifying such a valuation), Intel would be worth 1.4 trillion sometime in 2030.

Due to the risks involved, I think a very high discount rate of 25% is justified. It also makes me look less insane. This implies the Intel 2026 valuation should be $573B, or a $118 stock price! 😊

Now, for fun, let us throw in the Intel ASIC business growing to $15B. That is peanuts, of course, and I think Intel, with some more of Lip-Bu's hiring ability, could attract top SerDes talent, and so the ASIC business could be much larger.

I wrote a whole article about why Broadcom is screwing their customers as a middleman hated by everyone (all true, by the way), while MediaTek is causing delays for Google. Meanwhile, Google is gaining experience with EMIB, and Lip-Bu is making serious inroads.

For the Intel GPU business, I figure Intel has to at least secure 1 Gigawatt a year, which is probably $15B in revenue.

If we get both of those at a 40% operating margin, then we can add $12B in extra operating income.

Now, regarding TeraFab, if Elon gets 80K WSPM of 14A, I think a reasonable royalty for the IP is probably 25% of the wafer value. So, an annualized 80K WSPM * 32K equals $7.5B.

If we throw those in (some are more likely than others), the Intel operating margin grows to $65B. With a 30 PE ratio, that implies a 2 trillion valuation. That means Intel should trade today at $819B, with a $168 price target. I think we should shelve this one for now, but it is entirely likely to view this as a possibility when we have more visibility into these new businesses.

If you read this far, Intel should start additional shell construction in Ohio by 2026. DO IT

I also have a Substrate rant.

Personally, I suspect Intel will acquire Substrate, the XRL tool maker, in an all-stock transaction. The recent data seems to be quite good; something is going on there. If Intel got an exclusive FEL tool, it would gain a material cost and technological advantage over TSMC. I figure that if Substrate demonstrates their tool has no technical wall in front of it and could be HVM ready in the next three to four years, they would probably get taken out for at least $50B, maybe even $75B. If Intel did an all-stock transaction, we could see 20% dilution. However, that is still cheap when Intel could literally dominate the industry for the next decade while everyone else is stuck with LPP. It’s worth sinking some engineering time to know!

To make the acquisition cheaper, Intel and Micron could do a JV acquisition. Both get to use the tools for their respective businesses, since Micron would benefit from the tool as well. This might be a more palatable idea if Substrate really pans out and doesn’t sell super early. They might be worth north of $100B. I would advise Intel, if they think this will work, to BUY EARLY.

“This implies the Intel 2026 valuation should be $573B, or a $118 stock price“. Alex, if this happens, I am sending you a bottle of champagne. My EoY target is around $80, or $400Bn. I prefer yours though haha

Great analysis!