Intel Post Earnings

I’m gonna be lazy and not cite sources, but if you call me out on a claim, I will find a source and prove you wrong.

First off, looking at the Q4 numbers, they really weren’t that bad; it’s the guidance that people aren’t liking. Intel is citing a lack of supply, and it’s clear why.

Why This Happened

Intel made a fateful decision at the end of 2024 to do a tool write-down for Intel 7. They decided that Fab 42 was better off being upgraded to 18A to help lower CapEx numbers for the new node. At the time, this sort of made sense. If Intel didn’t do this, they would have had to run up inventory or lower utilization on products that it appeared people didn’t want. Intel really wants to show the Street that Foundry isn’t getting worse; if they hadn’t removed that supply, the depreciation without revenue would have made 2025 look much worse on paper.

The second factor is that Naga, who is running Foundry, is a memory guy. I think he’s great, but he lives on a “run it lean” mindset. In memory, when the market is lean, it’s a commodity, you just raise prices. In the CPU IDM business, you have OEMs. You can’t suddenly hand them an 80% price hike, especially when Intel has relied on them to carry products that were worse than AMD’s over the past few years. You don’t rat-fuck your customers.

So, what happened? In 1H 25, Intel started seeing Client OEMs demanding more Intel 7 parts due to tariff concerns and a desire to build cheaper PCs. At the same time, Intel talked to hyperscalers, and CPU demand for the data center didn’t look big.

So what did Intel do? They shifted capacity more towards Client Intel 7, expecting Arrow Lake and Lunar Lake to start falling off. Then, in the fall as Dave said on the call hyperscaler customers said, “Wait a minute, we need data center CPUs now“ (lots of demand reasons; this is gonna be yuge).

Intel tried to shift back to data center, but now they needed more Client products to fill the gap. Dave hinted on the call that they couldn’t get enough of what they wanted from TSMC (and those products have worse margins anyway), so now they are short on everything.

Intel was living off surplus inventory, and what Dave probably doesn’t want to admit is that they finally had to just let the dam break. No more holding back to keep numbers steady while hoping to essentially ride it out to the capacity bump. They had hoped to avoid this revenue air pocket entirely.

So what is Intel doing about this?

Dave said on the call that WSPM (Wafer Starts Per Month) is being added to Intel 7, Intel 3, and 18A every single month. The surprising part is that on the last call, Dave explicitly said they weren’t going to add to Intel 7.

Now, is Intel buying new tools for Intel 7? No way. I suspect they are looking around the factory network (Ireland or Oregon) to find tools that are underutilized and shipping them to Arizona to support Intel 7, or maybe grabbing used tools on the market.

Now you might ask: “If Fab 42 is supporting 18A, why is there a shortfall?” Two reasons. First, 18A requires a lot more steps, so your output per square foot is much lower. Second, Intel 18A wafers from Arizona aren’t being sold until Q2. They started HVM in late November/December. Three months later your wafers leave the fab, then they are packaged.

Third, there are so many morons on X who don’t understand how semiconductors work. First thing is that you need something called shell space, that’s the actual concrete building. That takes 3 years to build. Intel is swimming in shell space across every site. TSMC is out of shell space; when they guided CapEx, a lot of it was just for concrete. This is also why memory supply is not going up much they are out of shell space, and Micron has had to go out and buy an empty fab just to find room.

Next thing is, you actually need to buy the tools for this. Even if a tool is available immediately, it takes a minimum of 6 months after you get it on the floor to actually start driving your output higher. Intel is really only just now getting the tools it ordered in the past few quarters.

WHAT MATTERS FOR PRODUCTS

Most of this supply shit is noise; Intel revenue will climb as supply goes up. Lip-Bu on the call even told you that Intel will take Client share back with Panther Lake and Nova Lake, and the roadmap looks extremely strong. Lip-Bu doesn’t bullshit you, and no one should want Pat’s over-exaggerations back.

AMD’s internal marketing for client notebooks got leaked today, and it was desperate spin. They know they are cooked.

If anyone bought the stock for what Intel is going to earn this year, you are an idiot. What matters is that Data Center CPU demand is crazy. Dave hinted at multiple years of demand for what they see RIGHT NOW. That gives Intel time to get a competitive DC CPU like Coral Rapids out. We are lucky this is occurring. Intel can max-ship Intel 7 and Intel 3 CPUs despite them being inferior products. Great stuff.

FOUNDRY

On the call, you could tell Lip-Bu and Dave were pulling out big hints to get the market off the weak Q1 guide. This gives us a lot of red meat.

Advanced packaging deals are now billion-dollar opportunities each. Customers have prepaid for substrate, which is an effective lock-in—especially given the rumors surrounding TPU and Trainium 3.5.

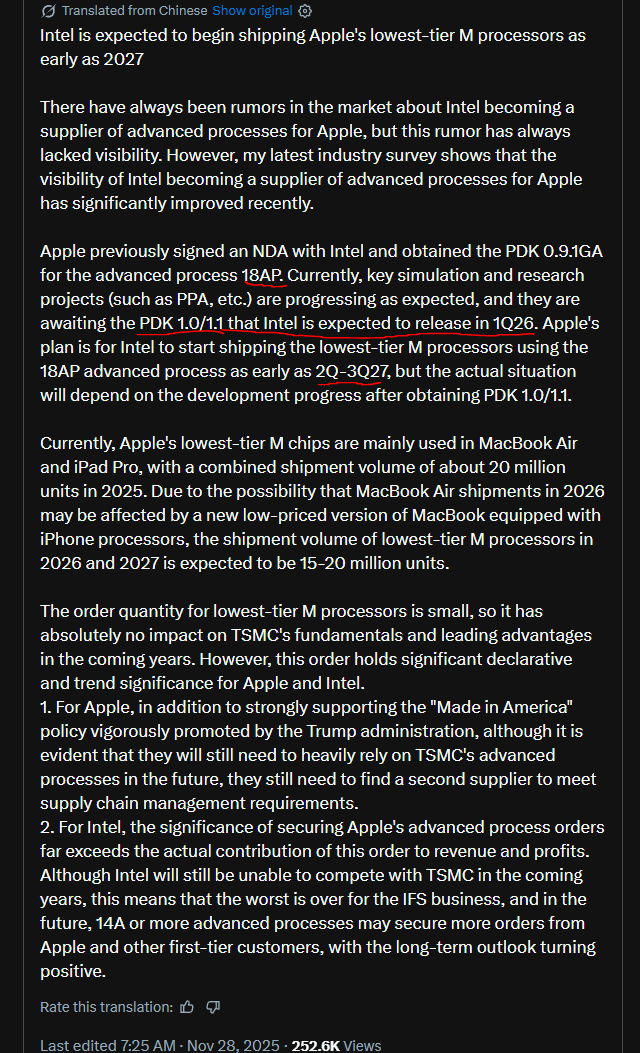

Lip-Bu also heavily hinted at an 18AP customer for this year right after the 1.0 PDK dropped at the end of last year. Well, I wonder who that might be?

In terms of 14A, Lip-Bu was quite positive and said customers would "finalize what volume." That wording is just Lip-Bu being sloppy; what he's really saying is that we already have the wins, but the customers haven’t given us firm volume commitments yet. Keep in mind, this is for 2028.

A fun hypothetical: let’s say Intel printed these exact results, BUT had added, “We have won the M-series chip with volume starting next year” (even if the actual revenue isn’t much). What does the stock do?

I bet the stock rips. Why? Because a major third party has finally blessed Foundry, and the TV pundits would actually have something positive to talk about.

Intel has won the M-series. Lip-Bu isn’t going to blab about it. Apple doesn’t want him to, and frankly, the actual volume required right now isn’t even that huge.

Intels ASIC Business

I’ll have to relisten to the call, but Dave said the custom ASIC business did $1B in revenue and grew 50%. That’s great, but what does the future look like?

Lip-Bu said he’s talking to hyperscalers all the time, and they are sharing what their workloads actually look like. He sounded extremely upbeat about customer feedback on what Intel can provide across ASIC, CPU, and Networking. Remember, Intel already makes custom network chips for AWS and Google.

Broadcom is hated by their customers, and MediaTek is sorta fumbling a bit. Intel provides everything a hyperscaler wants except memory. This is an easy W for Intel.

OVERALL

I’ve said after every selloff that the market overdid it, and I’ve kept buying. The same trends from yesterday remain true today. Intel is a fixed cost business unlike Nvidia. When your revenue goes up a bit, profits go up alot more!

Intel’s Client roadmap is set to steal share from AMD starting with Panther Lake. Data Center CPU demand is so high right now that Intel can ship less competitive products for the next ~18-24 months before Diamond Rapids and Coral Rapids get into volume. This is called being lucky—Pat never had this luck.

The 18AP PDK is healthy, and 14A remains on track. I believe they said the 1.0 PDK for 14A ships at the end of this year, with risk production in 2H 27.

Logic demand is absolutely bonkers, and supply from TSMC will be more limited for AMD than for Intel. Just because Intel can’t get enough supply for the next few quarters doesn’t mean shit about 2027 and 2028.

EMIB-T is superior to CoWoS; this is especially true when substrate is in short supply. TSMC wastes so goddamn much with a whole interposer. Intel uses a silicon bridge, not a goddamn wafer.

If you don’t buy into the story, sell and move on. Intels tailwinds are the future, fumbling Intel 7 supply is not a change in thesis. Just watch the guide for Q3 with increased supply and Intel ramping prices for data center cpu’s.

Plenty of people sold in the high 20s and 40s. Intel has 160K WSPM of blended leading-edge capacity with a price per wafer of ~$28K.

Do the god dam math yourselves

Great insights Alex

Right on the pulse!