Intel year-end wrap-up

Lip-Bu has delivered gifts for shareholders and tech enthusiasts alike. Where Intel goes from here to reclaim lost glory.

What a year. We started at $20.22 a share. The narrative was that Intel was a failed company; Qualcomm and Broadcom were circling like vultures, eyeing a giant still doing $50B in revenue but trading at a $100B valuation. The United States stood to lose its only chance at a true national champion and the home of Moore’s Law. A dear family friend of mine, along with 15,000 others in Oregon, faced the prospect of losing their jobs. America risked losing the ability to manufacture semiconductors independent of the goodwill of foreign countries—nations that would decide what node and capacity the US was allowed to build.

Thankfully, this did not come to pass. Instead, Lip-Bu Tan heard the nation’s call. He walked up on the Las Vegas stage to explain why he had joined.

Visibly choked up, he said, “I love this company... I simply could not stay on the sideline knowing I could help turn things around.”

I hope Tan stays around for a long time.

I also want to thank all the new Substack and Twitter followers who came along for the ride this year. For me, Intel is both an investment opportunity and a conviction; I passionately believe it is key to ensuring American power across the world. We invented the transistor, and Intel shepherded Moore’s Law. Why should we give up now when we have the world’s greatest fabless companies, giving us control over the demand that fuels TSMC?

The economic consequences of a likely war over Taiwan, which I believe will happen during Xi’s reign, are incalculable. Our government needs every tool at its disposal to push back against the growing threat of the PLA. Backing Intel to secure a dominant share of the foundry business is the only way to square this circle. This inevitability is a strong tailwind that will drive Intel forward for decades to come.

Intel 2026

Some things never change. Most Wall Street analysts still view Intel as a failed company and a toxic asset. I suspect Intel will remain toxic to the consensus even after the official foundry announcements. It will likely take Intel breaching its all-time high of $75.81 from August 2000, combined with a new government-sponsored shell expansion, to truly ignite interest. (I will go into more detail on this later in the article.)

When will Intel break its all-time high? 2026 is the year.

To understand the roadmap that will deliver the profits needed to justify such a valuation, we typically view Intel as two business units: Products and Foundry. However, I suspect that in the future, Intel will be seen as three distinct businesses: Products, ASIC, and Foundry.

First, let’s go over Intel Products

Today, Intel owns roughly 75% of the PC x86 market, with a higher share in laptops and a lower share in desktops. They also hold 50% of the overall server market. However, Intel’s share has eroded over the past five years primarily due to three factors:

Process Nodes (2020-2024): Fixed

Slow Architecture rollout (2020-2026): TBD

Lack of ‘X3D’ or large last-level cache (2020-2026): TBD

Let’s address the first point. Intel used to rely on monolithic-only designs built on its own process nodes. Under Intel’s famous “tick-tock” model, each “tick” was a new process node, and each “tock” was a new architecture. This two-year cadence allowed Intel to extend its lead to an unheard-of three years. By 2014, Intel’s 14nm was twice as dense as TSMC’s offering. Then 10nm happened, and everyone knows the story.

Intel has moved to a ‘tile’ design (or ‘chiplet’ for AMD fans). This was first seen on Meteor Lake, where the compute tile was on Intel 4 while the graphics and IO tiles were made by TSMC. Intel’s follow-on product, Arrow Lake, used TSMC for all tiles. These products have not been well received, primarily because Intel’s first attempt at tiles led to latency regression and suboptimal fabric performance.

Intel’s end-of-2026 product, Nova Lake, features a new fabric that largely resolves the poor latency seen in earlier products. Every tile on Nova Lake will be made by Intel except for the compute tile, which will use TSMC N2P. Intel has made a commitment to deliver the best product possible, and for the second half of 2026, that happens to be N2P.

On the second point, Intel has introduced only two substantive architectures in the last five years. We have seen Golden Cove and its derivatives since 2021; even today, the lead server product, Granite Rapids, uses a very similar derivative called Redwood Cove. Intel finally introduced a new architecture for Arrow Lake in 2024, ‘Lion Cove’, which will be used for two years.

Starting at the end of 2026, Intel will finally move beyond the necessary mess that “5N4Y” (5 nodes in 4 years) created. We will see the end of multiple nodes ramping simultaneously and the scattering of delayed products, replaced instead by a consistent yearly cadence.

Nova Lake starts Intel’s architecture sprint in 2026 with a new P and E core. Then, in 2027, Intel will release Razor Lake, featuring a new architecture rather than the small derivative changes we have seen in the past. Then, in 2028, with Titan Lake, Intel drops the P-core and moves to a ‘unified architecture’ where the E-core replaces the P-core. Intel’s current E-core shows remarkable performance for its size and looks much more like an ARM core than the traditional x86 P-cores from AMD and Intel.

Regarding the third point, Intel will deploy bLLC SKUs with Nova Lake that feature very large L3 caches to compete with AMD’s ‘X3D’ cache. Razor Lake or Titan Lake will then utilize Intel’s own 3D stacking technology, which is currently seen on its server CPUs to stack a large L3 cache.

Lip-Bu Tan has stated that Nova Lake is the most competitive PC part Intel has released in years. That is only the first product of the upcoming three-year sprint to retake the market.

On the server side, Intel’s management has indicated that its upcoming server CPU, Diamond Rapids, will not be as competitive as initially hoped. It will take until Coral Rapids before they believe share gains will return. Intel is very lucky that the current server CPU market is likely to remain hot through 2026 and 2027 due to AI Agents, AI RL, and a traditional server refresh cycle. (Seriously, if you have a job that uses AWS, you would be shocked at the amount of Cascade Lake that is still out there.) Initial leaks point to Coral Rapids arriving a year after Diamond Rapids for an end-of-2027 release. Theoretically, Intel would follow that with a unified architecture server product that would have much higher PPA, given what the current E-core roadmap looks like.

Moving onto the Intel Custom ASIC business, or ‘ICA’

I wrote a previous article that described what I envisioned for an Intel Custom ASIC division. (If someone at Intel reads this, feel free to take the name ICA😀)

We recently received news from John Pitzer that ICA positions itself as a competitor to Marvell and Broadcom. They are open to licensing or acquisition to acquire necessary IP if they lack it. Considering Intel used to own Altera and maintains a 5G telco business, they should already possess a competent and high-performance SerDes team and IP foundation. I am also pretty confident Intel is buying SambaNova; their design is FPGA and fabric-heavy, which suggests SambaNova has a strong SerDes team that Intel wants to bolt on.

What is not known to most of the Street or investors is that Intel has already made ASIC network chips for the hyperscalers. Intel has made custom IPUs for Google Cloud since 2022. They are currently making an IPU/Fabric chip for AWS using Intel 18A, and they are making an 18A product for Azure as well.

These relationships are key to winning business for ICA. Right now, Google has two partners for their TPU: Broadcom and MediaTek. MediaTek has delayed and slowed its TPU rollout, so I am honestly surprised the Street is actually bullish on them. Meanwhile, Broadcom is robbing Google blind. Lip-Bu Tan stated on the earnings call that customers he talked to are not happy with their current design partners. I suspect it’s Broadcom lmao.

Read my article to see why ICA can win; they lack the conflict of interest that everyone else faces since Intel is a foundry.

I suspect Intel will get a shot as a second-tier ASIC partner at Google, Amazon (currently Marvell and Alchip), or Azure (Marvell and GUC). From there, they will muscle their way into winning all three. Seriously, Intel just wants these guys in the Foundry; ICA is just the cherry on top. ICA also has opportunities to expand in its current segments, like CPUs and networking.

This is Intel’s ‘AI’ opportunity, given my personal view that ASICs will dominate later in the decade. Companies and people want tokens; they don’t care how they are created. Nvidia is likely to dominate the enterprise on-prem market given CUDA. However, Intel might be able to sneak in a low-power GPU (Crescent Island) for those not looking to get a one-megawatt rack and who don’t need pure latency and throughput.

Intel Foundry

This is the juicy part most investors are in the stock for. TSMC is a monopoly that brings in $100B in leading-edge revenue. Only three companies in the world will ever compete here (Sorry, Rapidus).

We recently got news that Apple will be using Intel 18AP for non-Pro MacBooks in 2027. I still suspect Intel can win a few more 18AP deals next year. Hyperscaler ARM CPUs come to mind, given that capacity constraints for N2 are likely to extend for a while.

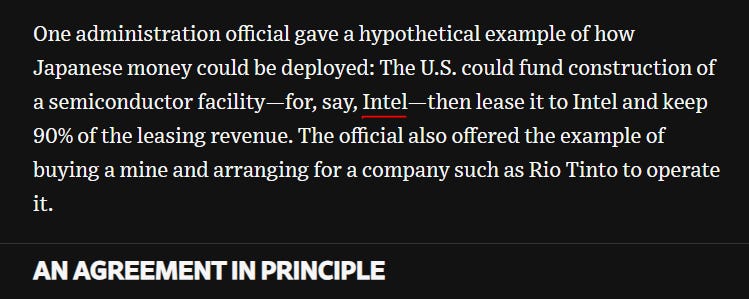

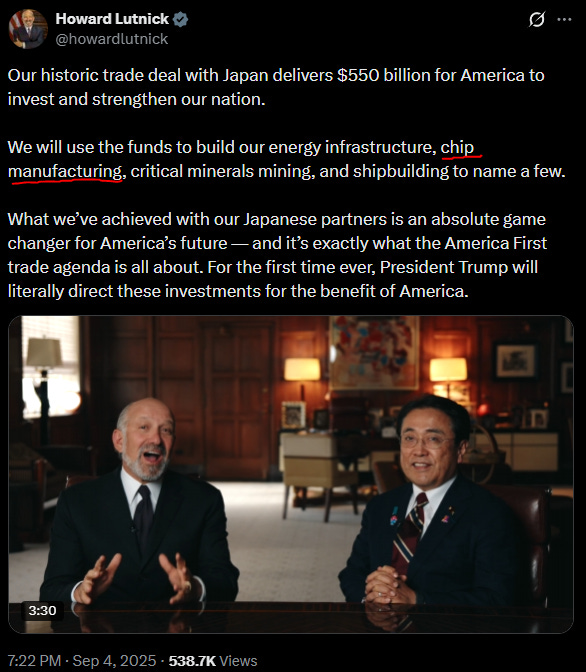

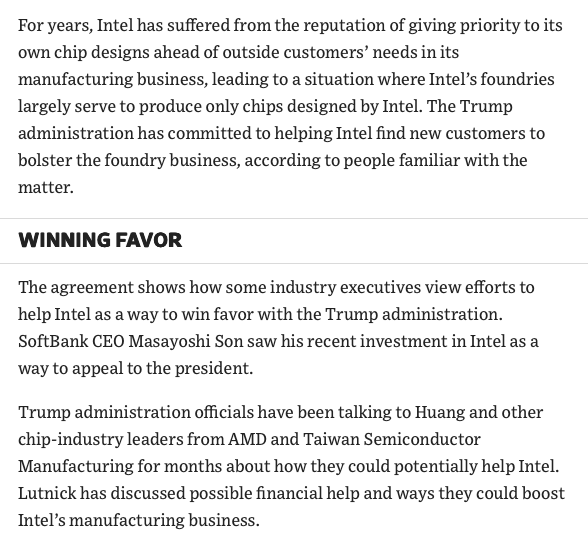

But clearly, the vast majority of Intel’s shell space in the future will be dedicated to 14A. I still believe, as was hinted in the WSJ, that sometime next year Intel will announce a ‘shell lease-back’ deal with Lutnick.

The Trump administration controls the $550B Japan fund, and both the MOU and related tweets explicitly mentioned semiconductor manufacturing.

This deal would involve the government paying for and owning the ‘shell’ (the building itself), while Intel would sign a long-term lease after construction. Currently, these shells have a 20-year deprecation schedule and take roughly four years to construct in the US. Intel will need more capital down the road to fill the shells with tools, but turning CapEx on zero-ROI buildings into OpEx via a lease will significantly help Intel’s cash burn until 2030, when these buildings are finally tooled.

Lutnick has also told tech executives about a “1:1” chip tariff and his goal of capturing 40% of the global market share for chip making. In an interview with NewsNation, he stated he wanted Taiwan and the US to split production 50-50. Taiwan later clarified that this was not acceptable. To achieve this level of share, Intel would need to construct a minimum of three additional shells, and more than likely would need to look at seven more in Ohio.

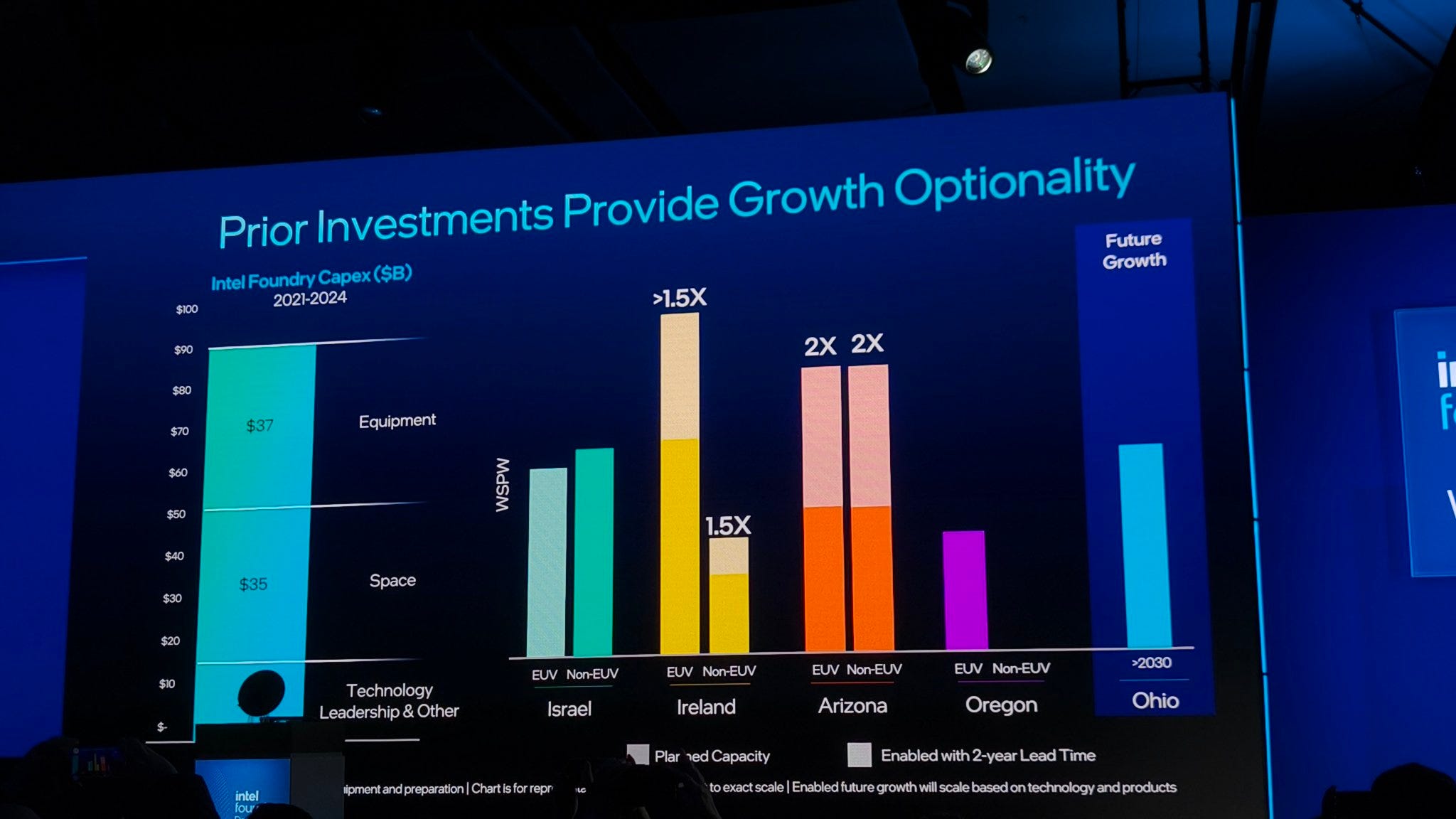

Currently, Intel operates with the largest unused cleanroom space in the industry. Let’s break it down

Israel Fab 38 sits with 685,000 square feet of empty cleanroom space. Intel Ohio could be accelerated—given its current construction progress—to 2028, adding another 685,000 square feet. In Arizona, Fab 62 adds an additional 342,500 square feet, while Fab 52 and Fab 42 have ample room to tool up for Intel’s current internal manufacturing needs.

Intel 18A did have some stumbles along the way. Risk production was originally targeted for December 2024 but slipped to late March 2025. Intel 18A also saw some performance targets pulled back and faced issues with frequency regression compared to Arrow Lake H (N3B) CPUs. Despite all that, Panther Lake on 18A achieves 10% higher performance and lower power than the previous generation on TSMC N3B (even compared to the monolithic compute tile of Lunar Lake).

Looking at the claimed performance and power efficiency gains, it is fair to ballpark 18A as equivalent to TSMC N3P. 18AP offers another 8-10% uplift, placing it near TSMC N2. Since 18AP enters High Volume Manufacturing (HVM) in Q4 2026, Intel is roughly a “half-node” off (approx. 5% speed difference) versus N2P in performance. Intel arrives just two quarters later in volume production, as N2P is slated to start in the middle of that year.

Intel is now closer to TSMC than anyone has been since 2017. Many new observers don’t realize that process nodes historically delivered a 50% speed uplift. This was common until the late 2000s; even Intel’s 22nm offered over 37%. So, when Intel was three years ahead of TSMC, they operated with a much larger lead than today’s competition enjoys.

Now, onto 14A. Lip-Bu Tan has stated that 14A is meeting internal milestones and is actually performing better than 18A did at the same stage of development. I had a nice Thanksgiving and heard similar sentiments from a very long-time process engineer at Intel who sold all their stock in 2014 because they saw the 10nm disaster coming. He is now optimistic about the current management and the recent changes after the layoff chaos settled.

Intel plans to reach 14AE volume production in the second half of 2028. Given current claims of a 15-20% improvement, Intel 14A should be roughly a “half-node” off (~5%) from TSMC’s A14.

A key detail to note is that Intel’s decision to go “backside power only” has made future shrinks easier. According to SemiAnalysis, Intel’s 14A M0 pitch is around the same size as TSMC’s N3 and N2 (since TSMC didn’t shrink much during the move to GAA). However, 14A can hit higher densities without TSMC’s aggressive pitch shrink. Beyond just HD/HP libraries, this increases effective utilization in actual designs, further improving real-world density. Intel decided to be first on backside power and has already taken its medicine on the teething issues during 18A.

TSMC, meanwhile, will be shrinking one of the hardest parts of the transistor for their A14 node, while holding only a slim PPA lead. TSMC will also be using backside power for the first time on A16. A16 is not a backside power-only node and is very expensive. In contrast, Intel started with PowerVia and moved to PowerDirect for 14A. I am very thankful Wei-Jen Lo has joined Intel to ensure PowerDirect goes smoothly.

Intel’s John Pitzer has said that 14A customers will firm up over the next 6 to 12 months. This is Intel’s biggest catalyst by far, since 14A external volume will dwarf any 18AP deals. (Though make no mistake, those 18AP wins still confirm Intel is right up there with TSMC and will drive sentiment and the stock up significantly.)

I think by the end of Q2, we will get our announcements. Alternatively, if Intel decides not to publicly name names, announcing a large CapEx increase would be enough to confirm demand is there.

Don’t guide 2026 CapEx in the Q4 call, Dave!

Intel will also reaccelerate Ohio’s construction as a tangible sign of demand. This is politically critical for Republicans heading into the 2026 midterms. I suspect that a portion of the orders for the Ohio fab will be driven by customers looking to avoid tariffs (where domestic orders effectively act as rebates). This narrative is key for the Trump administration to claim success, especially given the lingering perception in the community that Intel Ohio is a “boondoggle. The Trump adminstration needs a strong Intel to reach their goals, and is currently out there peddling business to them.

Conclusion

Intel will surpass its year 2000 high next year, primarily driven by foundry deals. We need to see 18AP deals and very large 14A deals materialize. Pitzer said it’s a matter of ‘when,’ not ‘if,’ and I am sure the Trump administration agrees. Intel is back on track with process nodes and is hungry to deploy its advanced packaging more broadly (offering EMIB with capabilities similar to CoWoS).

Intel is ready to win business in this tight, leading-edge market, especially from customers needing to avoid tariffs. Intel 14A marks the first node where the company effectively stands toe-to-toe with TSMC. Lip-Bu Tan is an execution machine.

Sources:

https://www.wsj.com/politics/policy/sovereign-wealth-fund-japan-trade-deal-b0fadb1a

Intel Foundry Day 2025

Banger!! Amazing year end post. Thank you for being the voice of reason when wall st cant understand the story.