Previewing Intel's Q2 Results

Internal demand is skyrocketing, Intel's lead contractor for Ohio is on a hiring spree, and Lip-Bu just hinted at how external foundry volume will ramp (IDM is back)

Intel guided Q2 to $13.8B–$14.8B with an EPS of $0.20.

They’ll probably beat that, given the upbeat language from Dave and Intel’s now-consistent approach: promise less, deliver more. Ultimately, these numbers don’t really matter.

What matters is what has happened since Q1. Mainly, internal demand drivers are up a lot.

Internal Demand

Lip-Bu on the No Priors podcast gave away what Intel’s mix is going to look like for the foreseeable future, and IDM is back. Specifically, he said, “my Foundry” (meaning external customers) really takes off in 2030, 2031, and 2032. He also mentioned talking to the board about going much “bigger”; given where Intel’s stock price is today, Intel has to start planning on becoming a much bigger player.

Now, if you can’t see the full picture, your reaction might be: What! Is Intel Foundry delayed? But in reality, Intel is seeing a massive reversal of fortune.

When I initially wrote my first Substack (and tweets, too), Intel’s internal demand could roughly be thought of as holding steady while transitioning to new nodes. There was no real wafer growth, and the GPU strategy seemed to be in no man’s land.

That’s not the case due to three factors this year:

CPU demand is 4–5x market expectations compared to 2025 (jumping from $40B to $200B+).

Wafer supply went from loose, to tight, to now multi-year tight. AI inference is so hot that pretty much any chip will sell.

Lip-Bu and Kevork have stated that the DCAI plan relies exclusively on Intel Foundry. Lip-Bu is also doubling down on GPUs: “I’m quietly building my GPU team” (Intel GPU hiring is going crazy, and recent hire Eric Demers leads the effort).

These drivers mean Intel doesn’t need to go find a 40–50K WSPM customer on 18A. It also means Intel can get their foot in the door for GPUs compared to Gaudi, since they control their own destiny on wafers. Jaguar Shores / Shores Next in 2028/2029 is when substantial DRAM supply comes online and allows Intel to actually get their products out.

According to SemiAnalysis, Intel’s ramp is for 110K WSPM on 18A. Intel should be modeled as running at capacity in 2029/2030. The debate is around the Foundry split and how much is CPU vs. GPU/ASIC/Other. I’d lean toward a very, very heavy IDM mix given Intel’s comments around stabilizing CPU market share (AMD’s ramp is huge, so to hold is crazy). Furthermore, Lip-Bu’s optimism on GPUs and the current hiring spree indicates far more GPU volume than I think the market expects (like zero? lol).

Intel is going to primarily use their current shells for their own products and strategic Foundry customers. For example, known 18A wins include Apple’s A and M series (smaller volume). Additionally, there is a Marvell switch for Google, and Nvidia is rumored to be using 18A for its Rubin consumer GPU line and potentially for IO dies on Feynman.

These are smart wins and represent decent combined volume (20K WSPM?), but they aren’t huge. The vast majority of this 110K WSPM pool is Intel.

Intel’s major issue was funding 14A. We know that Intel’s lone product on 14A is a pipe-cleaner 2-core tile for Razor Lake, while the higher volume part, Titan Lake, is on 18A-U. Intel didn’t have someone to take the first 30K WSPM of 14A until their own demand arrived in 2030. A two-year hole that plagued management in 2025.

Well, Apple has filled that hole. They are going to take a big chunk of that 30K WSPM gap, I’d guess somewhere around 20K WSPM of 14A. This means 14A’s first real volume product is the iPhone. Thanks, Tim.

The next 14A customer is SpaceX; Jeff Pu has talked about a MediaTek AI inference ASIC for SpaceX fabbed on 14A. That order will be smaller, but a couple of gigawatts is still good (55K wafers per gigawatt).

Ohio Mod 1 and Oregon will be enough to get to 40K WSPM, and depending on the 10A ramp, Intel could hold 14A longer in Oregon, meaning Ohio + Oregon gets you to 50-60K. In addition, depending on Intel 3 demand, Ireland could begin to roll off in 2031, allowing for additional 14A supply.

Best Guess of Intel’s Manufacturing Network

To hit 110K WSPM, Intel will have to be creative and aggressive with their own customers to force them off Intel 7.

Fabs 42, 52, and 62 on their own can get Intel to 55K WSPM of 18A. Intel then needs to be aggressive in deramping (Non-EUV) Fabs 32 and 22 to push output to near 80K WSPM of 18A with the uplift.

Due to the ramp in server CPUs, Intel 3 production in Ireland might not be enough to cover all the base tiles used in Diamond Rapids, Coral Rapids, and Jaguar Shores. Intel 3 is also used for IO tiles in consumer parts going forward.

Intel’s remaining free fab is Fab 38 in Israel. Due to the Iran war, Intel has to be careful. Therefore, with the extra need for Intel 3 and 18A, I can see Intel potentially splitting Mod 1 to Intel 3 and Mod 2 to 18A.

Mod 2 with 18A, plus support from a deramped Fab 28, should be enough to lift 18A to 110K WSPM across Arizona and Israel. It’s entirely possible Ireland can produce Intel 3 to enough wafers, and with some design choices, Intel can free up some Intel 3 capacity, allowing Fab 38 to be dedicated entirely to 18A. But for now, assume Mod 1 goes to Intel 3 to allow for sufficient Intel 3 output.

For 14A, Ohio and Oregon will be the main drivers. Intel needs a lot more 14A capacity, and 18A is not rolling off due to 18AP-T demand. I expect several more shells coming soon to support 2030+ 14A demand.

It is funny that Dave Zinsner at the BofA conference said they are happy that Intel has shells coming online in 1-2 years, which he noted were once viewed as “boat anchors” and now going to be extremely helpful. This was obvious last year, and it’s why I continue to say Intel needs to start building more shells soon.

I haven’t mentioned Brookfield, which of course eats 50% of the revenue from Arizona. However, unlike Ireland, this arrangement has an easier out. Intel can buy them out at any time. I suspect that since Fab 62 is being readied for volume next year, Intel might buy out Brookfield ($7–$10B if they don’t buy more tools than currently) by Q4 or early next year. You should not model Intel long-term as having Brookfield; it’s a fool’s errand.

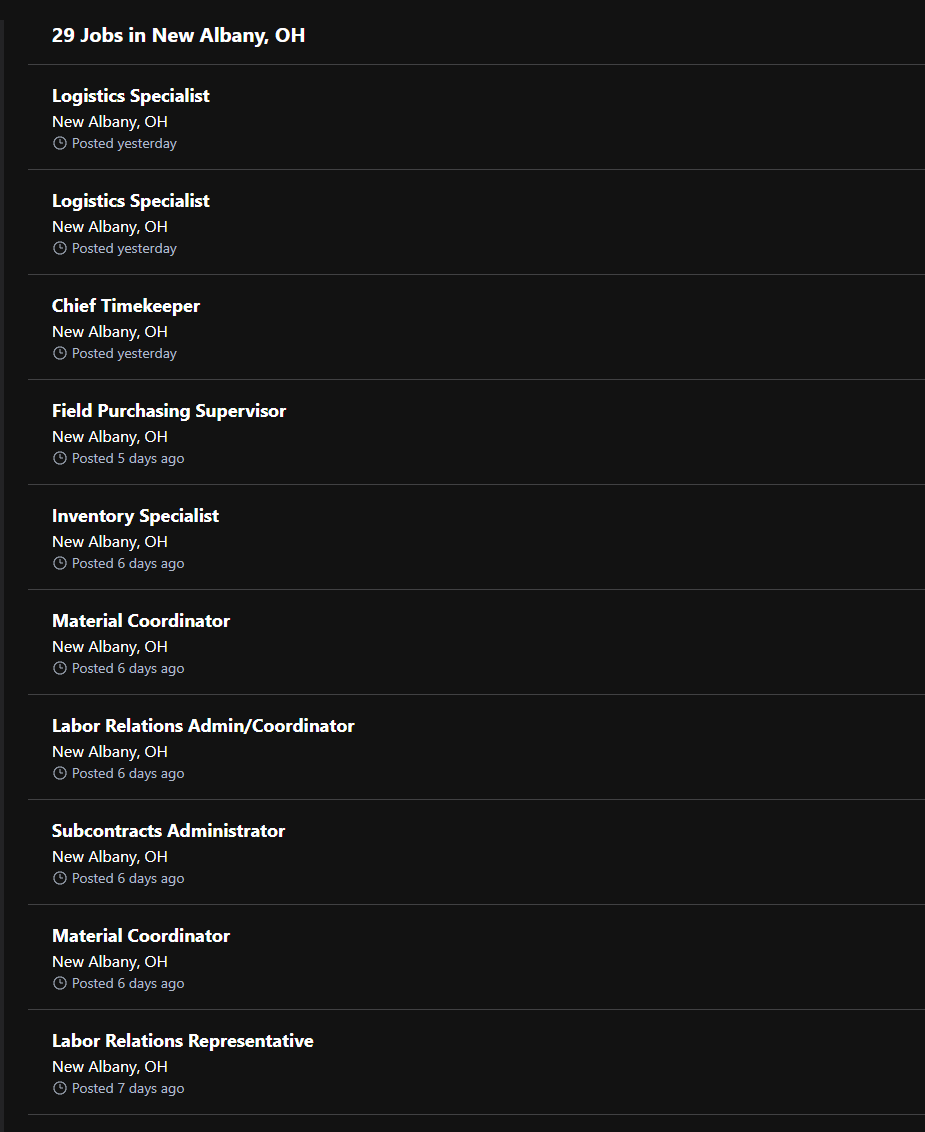

Ohio Job Postings

Bechtel is the contractor for Intel’s Fab 27 in Ohio, and I’ve been watching their job postings for the past 18 months. Usually, you’d just see a few listings pop up here and there. But over the past two to three weeks? It’s been an absolute torrent.

View for yourself:

https://bechtel.dejobs.org/locations/new-albany-oh/jobs/

We also know that during the Morgan Stanley roadshow, they explicitly said Ohio would be accelerated. However, Intel has not said anything publicly. I presume they will announce this as part of Q2 earnings. Weirdly, this has not been picked up in the press or on the newswires. I mean, Intel’s management talked directly to these guys? And said this, I’m surprised Ohio media hasn’t had a field day. I also believe Intel needs to start selling Ohio harder to Trump, just to get the talking point out there more regularly.

Final Points

Anyone who has paid attention can see this coming. But trust me, when Intel announces Ohio and possibly more shells (though I would guess that’s more of a Q3/Q4 announcement, which I hope it isn’t), people will be surprised. I also suspect the same thing will happen when analysts and investors realize Intel the IDM is back. This wafer shortage is a prime opportunity to grab GPU/ASIC share and stabilize CPU share (Intel’s management told Morgan Stanley that CPU share loss could stop by Q4 of this year, which is crazy). Then, they can onboard strategic customers with lower initial volumes, and hockey-stick that volume later when Intel is on better financial footing. That approach is much better for short-to medium-term earnings power, and it doesn’t reek of a need for do-or-die customers (outside of Apple thats do or die).

When Lip-Bu stated that Foundry really inflects in 2030+ and the board wants to go “big,” he’s setting Intel up to be a major foundry player longer-term. With TSMC tracking toward 500K+ WSPM of leading-edge logic by 2027, Intel needs a lot, and I mean a lot of capacity. Let’s go big. A CHIPS Act loan, prepays, and a capital raise are all OK by me.

Great post as always, Alex_Intel_! I’m strategically taking some rest and vacation over the summer from flying because I know it’s going to be a whirlwind after ~October. Years of drone flights over Intel Ohio are still to come.

The goat! Great analysis. Thank u